THE STATE OF THE HOUSING MARKET IN SUMMER 2025: INSIGHTS FROM OUR MARKET INTELLIGENCE WEBINAR

The U.S. housing market in 2025 is defined by complexity, caution and a lack of urgency among consumers. During our August Market Intelligence Webinar, Zonda Chief Economist Ali Wolf provided her analysis of the current housing and building economy and revealed both risks and opportunities for builders as they navigate an uncertain environment.

A SLOWING BUT GROWING ECONOMY

Wolf described the broader economic backdrop as a “slowing but growing” economy with mounting risks. On the surface, several indicators remain positive. Incomes continue to rise faster than inflation, consumer spending is holding at modest but positive levels and long-term wealth growth from the stock market provides a measure of stability.

However, underlying weaknesses are beginning to show. Housing starts have slowed significantly, which carries wider economic implications because new home construction generates jobs and fuels related industries. Inflation is also not yet back to the Federal Reserve’s 2 percent target, leaving policymakers in a delicate position.

Consumer confidence has improved since the spring but many households remain cautious about the next six months, particularly with regard to the labor market. As a result, builders are expressing more concern about consumer demand for new homes.

LABOR MARKET UPDATE AND ITS IMPACT ON HOUSING

The labor market has traditionally been one of the most reliable indicators of housing demand yet signs now point to a slowdown. Businesses are adding fewer jobs and are less willing to backfill open positions, leading to slower job growth overall. High-income job growth, a particularly important factor for housing sales, has turned negative in half of the nation’s top markets. This weakening trend has already contributed to more cancellations in new home communities as prospective buyers face job losses or feel less secure about their future earnings.

Regional variation remains important. The Carolinas, including markets such as Raleigh, Charlotte and Charleston, continue to perform relatively well compared to other parts of the country. By contrast, major production markets such as Dallas, Houston, Jacksonville and Las Vegas have experienced notable decelerations in job growth. These local labor market shifts directly affect builders by influencing demand, affordability and buyer confidence.

MORTGAGE RATES: A COMPLICATED BRIGHT SPOT

One area that has provided some relief is mortgage interest rates. After hovering in the high sixes to low sevens earlier this year, the average 30-year fixed rate has recently eased into the mid-to-high six percent range. While affordability remains strained, this marks the lowest point for rates since late 2024.

For builders, mortgage rate buydowns have become a critical tool for keeping sales moving. Wolf illustrated the trade-off between rate buydowns and price cuts with a striking example. Reducing a $500,000 home’s mortgage rate from 6.75 percent to 4.75 percent saves the buyer about $500 per month but costs the builder between $32,000 and $40,000. Achieving the same monthly payment relief through a price cut would require lowering the home price by $100,000. While buyers tend to focus on sticker price, the math makes clear why rate buydowns have become such a widespread strategy.

SALES TRENDS: INCENTIVES HELPING

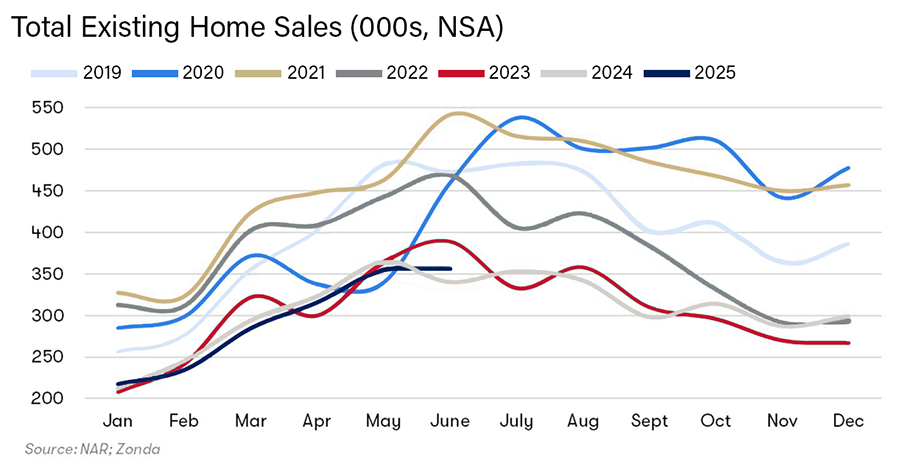

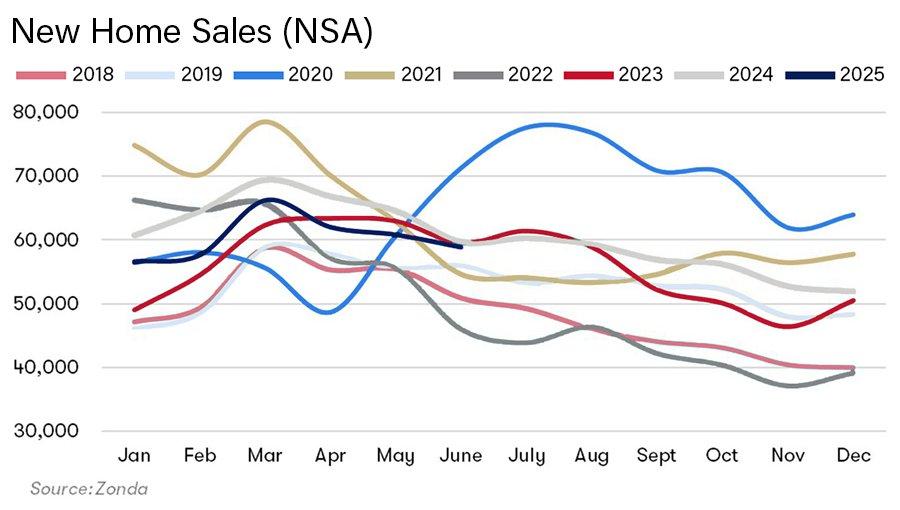

Both new and existing home sales remain under pressure. Existing home sales continue to hover at historically weak levels, essentially “bumping along the bottom.” The new home market, which had held up better in recent years, is now weakening as well. Builders often describe today’s environment as feeling similar to 2022 when higher interest rates and economic uncertainty forced them to use aggressive incentives just to keep buyers engaged.

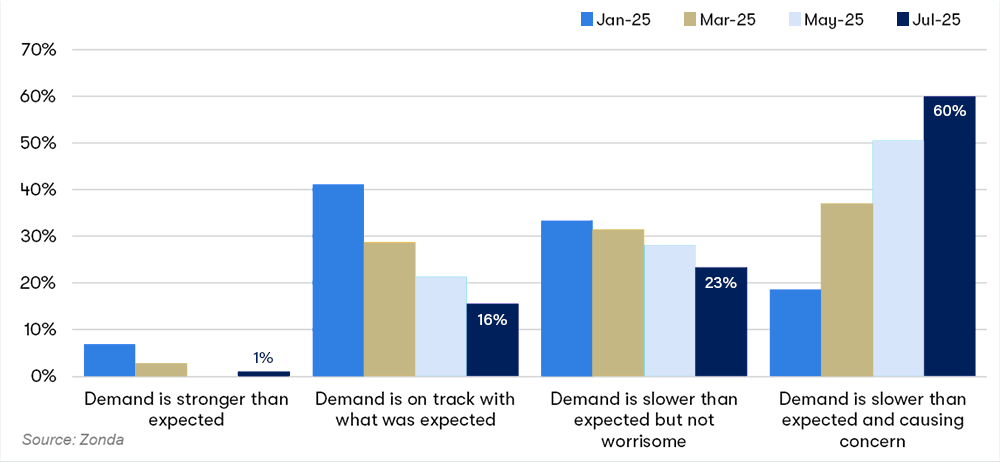

Price cuts are increasingly common across the country with some markets already seeing closing prices fall as much as 20 percent from their peaks. Incentives such as design credits and closing cost contributions are no longer seen as perks but rather as standard expectations among buyers. According to Zonda’s latest survey, 60 percent of builders now describe demand as slower than expected and concerning—triple the number feeling that way at the start of the year.

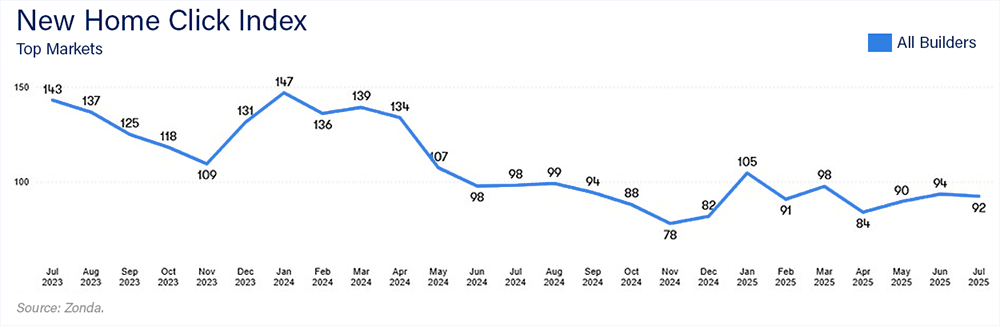

Another telling indication of the public’s lagging demand for new homes is in their internet search activity. Zonda’s New Home Source is showing a 5.8% decrease in click activity compared to a year ago. Fewer consumers are actively planning to buy a home on a national level.

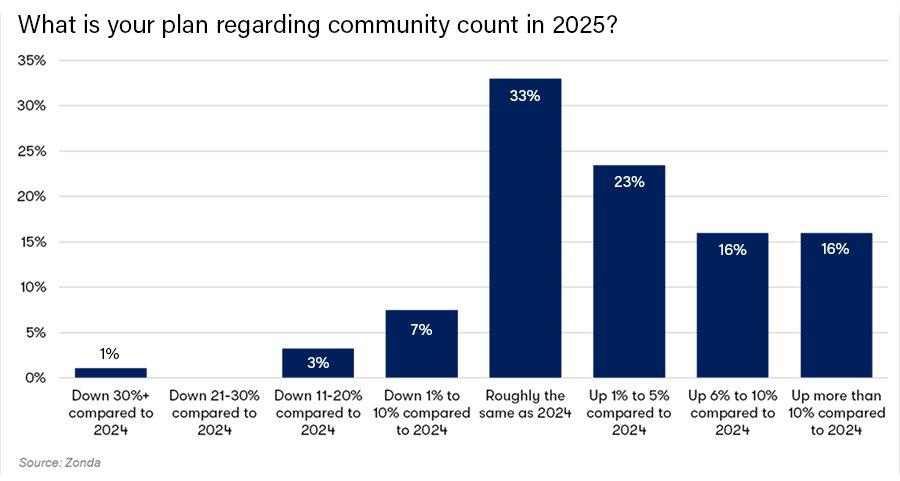

INVENTORY AND COMMUNITY DEVELOPMENT

Inventory levels are also shifting. For six consecutive months, there have been more new communities opening than closing, although the national count of active communities still lags far behind 2019. The contrast across regions is significant. In California, active new home projects remain 50 percent lower than before the pandemic, reflecting slower development activity and regulatory challenges. Meanwhile, Florida has 50 percent more projects than in 2019, underscoring the surge of construction in high-growth Sun Belt markets.

Most builders are not planning to halt new community development altogether despite slower sales. Instead, many are choosing to moderate the number of speculative homes they start in each community. This more cautious approach reflects a growing sense of discipline, with builders waiting to see how demand evolves before committing to larger volumes of construction.

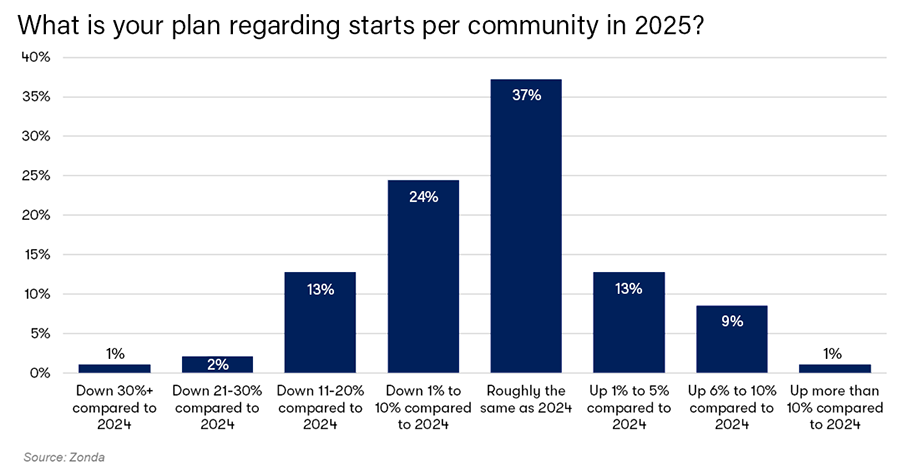

HOUSING STARTS: BUILDER DISCIPLINE PREVAILS

Perhaps the most telling indicator for the construction industry is the outlook for housing starts. Single-family starts are projected to decline by about 12 percent this year, a reflection of weaker sales and rising standing inventory.

While these numbers suggest contraction, Wolf emphasized that builder discipline is a silver lining. Unlike past cycles, builders are adjusting production to align closely with sales, reducing the risk of large-scale overbuilding. This more measured approach should help prevent the type of inventory glut that prolonged recoveries in earlier downturns.

WHAT IT ALL MEANS FOR BUILDERS

For builders, today’s market demands both caution and creativity. Incentives such as rate buydowns are essential tools for addressing affordability challenges but they must be deployed strategically. Close monitoring of local labor market trends is critical since high-income job growth—or its absence—often signals future demand shifts. Builders should also recognize the increasing regional divergence in conditions: while markets in Florida, Texas and the Mountain West face oversupply, others such as the Carolinas and coastal metros remain relatively resilient.

By maintaining discipline on starts and adapting to shifting consumer expectations, builders can position themselves to weather current challenges and capture growth when conditions stabilize.