MID-2025 HOUSING MARKET UPDATE

In mid-2025, the U.S. housing market is persevering through a challenging period. Despite certain economic positives including job creation and consumer spending, there is still concern in the air due to inflation, interest rates, home prices and rising construction costs. For builders, working successfully in this environment requires agility, a sharp eye on regional trends and realistic expectations for pricing and housing starts.

INTEREST RATE OUTLOOK

Mortgage rates remain higher than desired. There are several factors contributing to this, but Wolf believes the primary drivers are ongoing inflationary pressures and investor uncertainty toward the larger economy. Interest rates sometimes go down as economic uncertainty rises, but the factors pushing them up, such as inflation, government policy, rising debt levels and a selloff of bonds, continue to keep rates elevated.

While it’s impossible to know what will happen to mortgage rates at any point in the future, especially given the frequency of tariff policies changing, Zonda predicts they will continue to hover in the 6–7% range, marked by ongoing volatility. Builders should be prepared for price-sensitive consumers who may be shy about committing to a new home purchase in the current environment.

SINGLE-FAMILY HOUSING MARKET

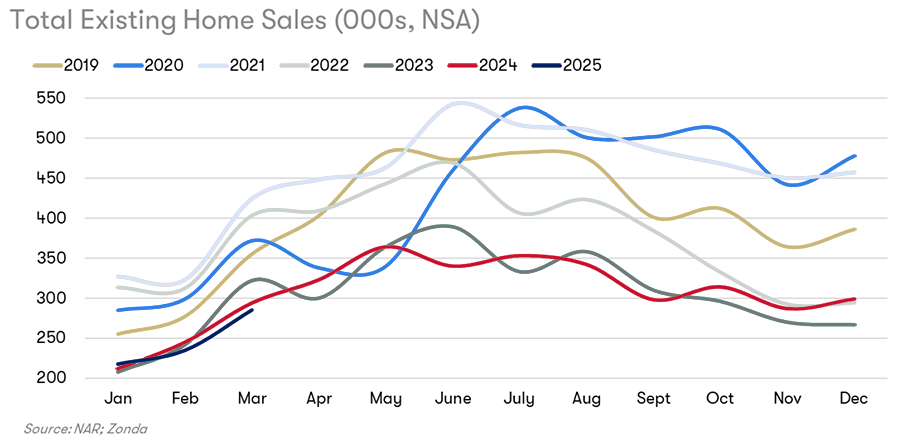

A major shift in the 2025 housing market is the disappearance of buyer urgency. Potential buyers are hesitating due to economic uncertainty, rate volatility and high prices. Existing home sales have dropped 3% despite a 30% increase in listings, highlighting that increased inventory alone isn’t enough to boost demand.

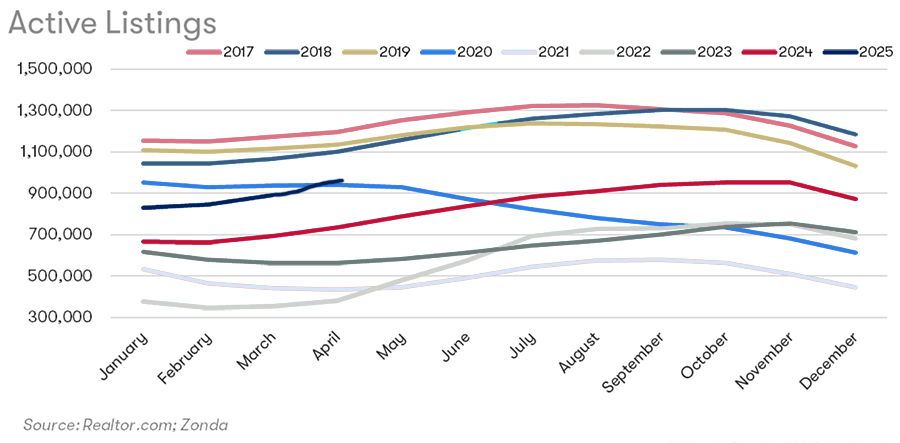

One particular bright spot is that, for the first time since the pandemic, a majority of the nation’s top markets have higher levels of inventory than in 2019, with the strongest increases in Florida, Texas, Colorado and Utah. Over the last five years, supply has been tight everywhere, so positive trends are appearing in some areas.

Also, it was a seller’s market everywhere five years ago. Now, different areas face different situations. Areas along the West Coast, Midwest and Northeast still qualify as seller’s markets, but more markets are now considered more balanced, which means they have four to six months of supply available. It should be noted that many of Florida’s listings are due to condos going through reassessment fees, which impact the overall housing market in the area and make it more of a buyer’s market.

NEW HOME SALES

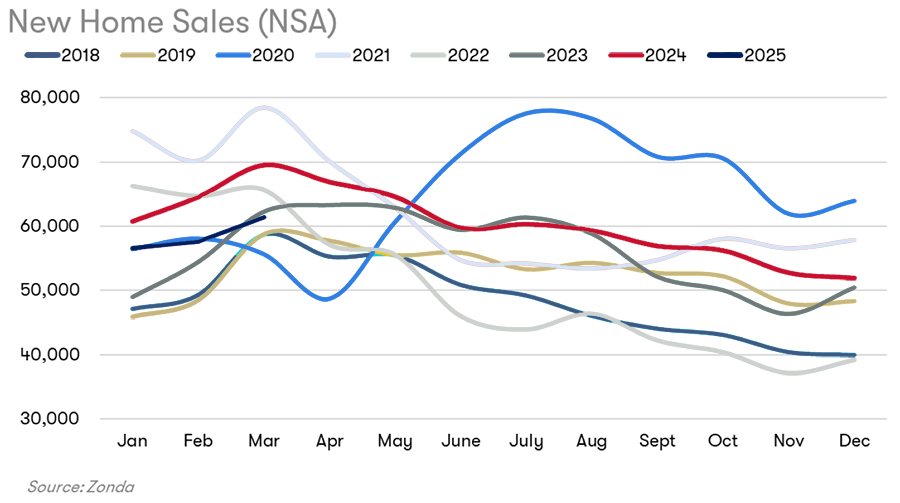

New home sales are still above where we were in 2019, but below the last couple of years.

Zonda’s Market Ranking (ZMR), adjusting for supply and seasonality, indicates:

- 40% of markets performing above average

- 34% underperforming

- 26% maintaining average performance

Builders nationwide regularly use incentives to attract buyers, especially in areas with the most resale supply because of the added competition. However, while incentives remain critical, they’re not as effective at driving urgency as they have been in the past. Common incentives such as mortgage rate buy-downs no longer strongly influence buyers. Today's buyers increasingly request personalized incentives, including design credits, closing-cost assistance and outright price reductions.

Zonda emphasizes that incentives are often underreported, as builders frequently offer non-advertised, individualized deals.

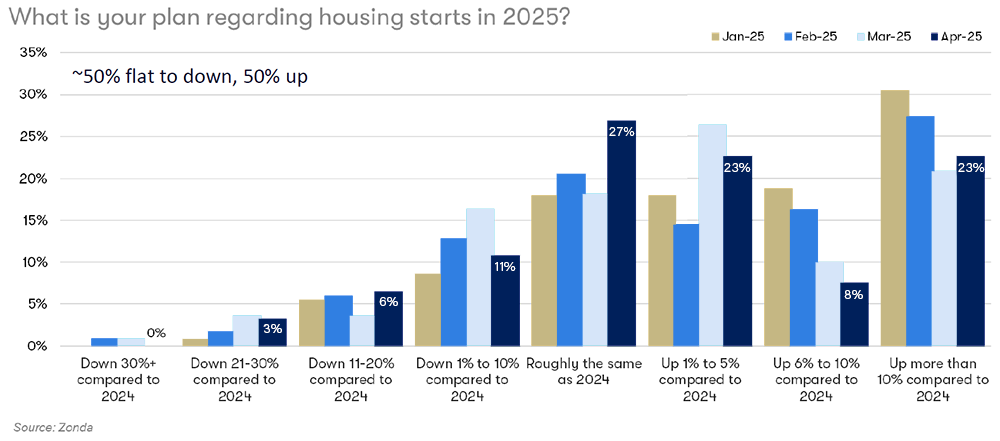

HOUSING STARTS FORECAST

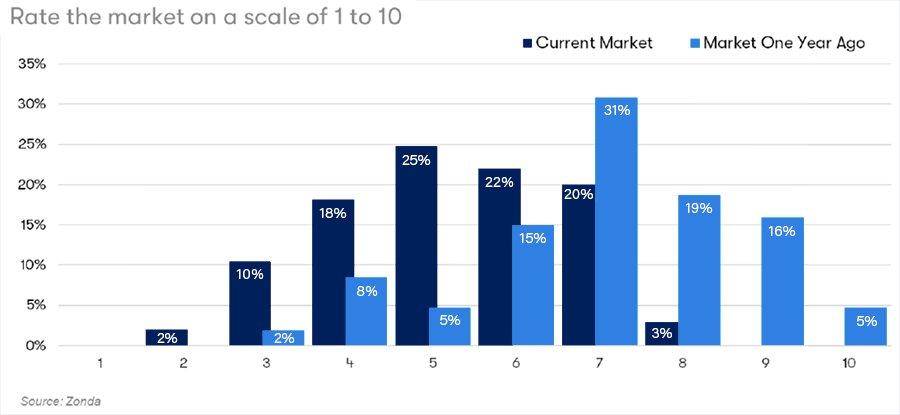

Builders rated market conditions at 5/6 out of 10 in the spring, down from 7/8 a year ago, though they expect a slight improvement in the coming months if current uncertainties in the economy are resolved.

Builder optimism regarding starts has declined overall, though many builders still expect to increase starts. Initially, the largest share of responses to Zonda’s survey projected more than 10% growth this year, but now the largest share expects roughly flat numbers. 54% of respondents still expect starts to increase by varying amounts.

As a result, Zonda revised its single-family housing starts forecast to -5%. This change reflects several factors:

- Pullback in spec starts

- Challenges in top markets

- Slower consumer demand

- Caution against oversupplying in an uncertain market

- Increased costs without being able to raise home prices

Builders continue to cautiously expand communities but remain wary about aggressive growth until market conditions stabilize.

DEMOGRAPHIC TRENDS FAVOR LONG-TERM STABILITY

Long-term demographic trends remain strong for the housing market. Millennials and Gen Z continue to mature into homeownership roles, and baby boomers, currently cautious, will likely return once market conditions stabilize.

Also, new homes now cost just 3% more than resales, down from a historical 20% gap, making new builds increasingly attractive. Major selling points for homebuyers are the ability to customize a new home and the peace of mind that comes with not worrying as much about the maintenance that often comes with older homes. New homes also generally feature lower insurance costs, and the incentives a buyer might receive from builders can make new homes financially appealing.

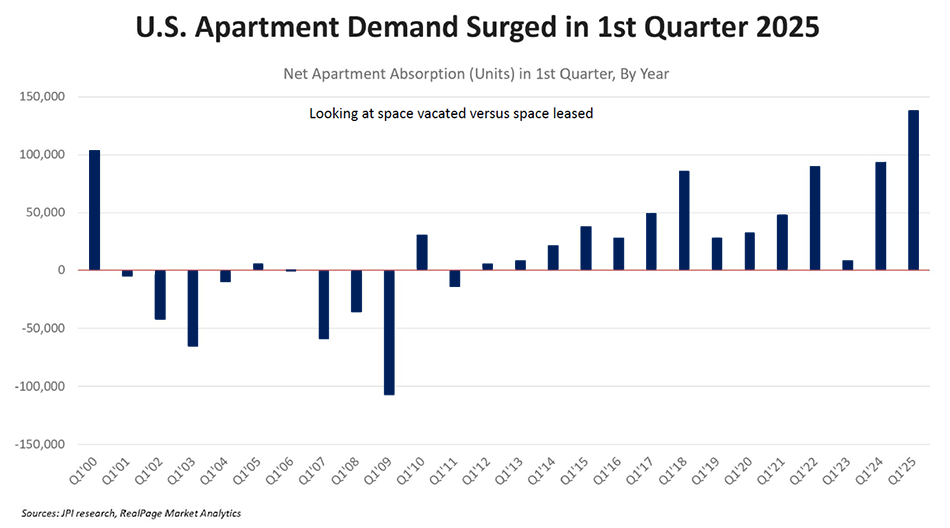

MULTI-FAMILY RENTAL MARKET

Apartment demand has been strong recently, which is helping to fill the oversupply issues hampering the multi-family sector.

Typically, developers want to have their communities at 95% occupancy, which is happening in certain regions, including areas along the West Coast and Northeast, but many areas throughout the Sun Belt are still below that threshold. With that being said, these numbers look much better than they did six months ago due to the increased demand, which is important to ultimately make the market more stable.

Multi-family starts remain modest, and the pipeline of new apartments may not see a full rebound for a while. However, there remain signs for long-term optimism. Zonda is revising their forecast for housing starts to be up 7%, which is great, but it’s just to a total of 360k, so there is still significant room for growth.

STRATEGIC RECOMMENDATIONS FOR BUILDERS:

- Monitor and protect margins. Use incentives carefully and strategically.

- Watch local market inventories closely. More markets are shifting toward balanced or buyer-driven conditions.

- Stay informed on policy changes. Tariff, immigration and zoning policies can shift rapidly, affecting operations.

- Anticipate delayed market recovery. Stability may not return until 2026; manage expectations accordingly.

- Focus on brand differentiation. With fewer buyers and starts, distinct branding and value propositions become crucial.

Stay tuned to Builders FirstSource for more market intelligence webinars, and be sure to stay in contact with your local BFS team to help you in any way.